The intersection of financial services and technology, or fintech, is where many people now go to spend, borrow, borrow, invest and trade. And they do that as second nature. Fintech makes financial services more efficient and adaptable, more personal and inclusive. Whether buying a cup of coffee with a credit card stored on a mobile device or splitting a dinner bill with Venmo, fintech applications are transforming the way businesses and consumers manage their finances.

We expect that as technologies like these mature and their adoption increases, prominence of the Fintech megatheme in investment portfolios will increase, and for good reason. Exciting opportunities continue to arise as Fintech, including the Blockchain theme, increasingly overlaps with emerging themes such as the Internet of Things (IoT), Cloud Computing and Video Games.

Key learning points

- We expect the digital transformation to bring financial services, including mobile payments, online banking and alternative lending platforms, to previously non-banking and underserved populations.

- The pandemic has accelerated the adoption of fintech, with digital payments becoming widely accepted. Key avenues for future growth include buy now, pay later (BNPL), cloud banking and blockchain-based segments.

- Traditional financial services firms continue to invest significantly in fintech as consumer demand for the convenience and convenience of these technologies increases.

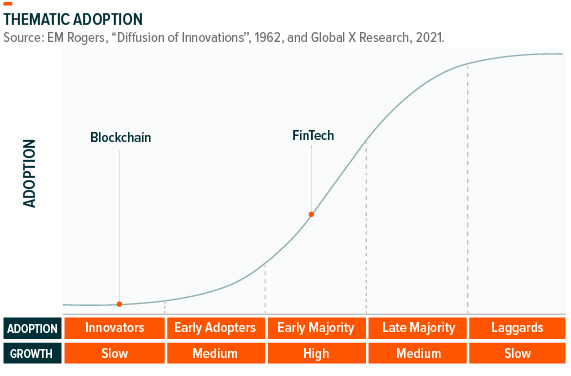

Fintech adoption gains momentum and becomes the norm

The adoption of fintech has skyrocketed in recent years and we expect innovation in the space to continue to broaden access to the global financial ecosystem. Global fintech investment activity, including through venture capital, private equity and mergers and acquisitions, accelerated from $148.6 billion in 2019 and $124.9 billion in 2020 to $210 billion in 2021.1

For consumers, the ease and convenience of purchasing goods or services by tapping a device at a point of sale makes digital payments the most recognizable segment of Fintech. For businesses, in addition to the initial cost of developing the program and infrastructure to execute transactions, mobile payment technology is a consumer-friendly way to keep ongoing and variable costs low. As consumers become more adept and willing to shop online, more integrated shopping ecosystems are developing. The success of Fintech’s fastest growing segment, BNPL, is the result of continued growth in online shopping.

Overall, US consumers using fintech grew from 58% to 88% between 2020 and 2021.2 In comparison, it took the refrigerator 20 years to reach a similar level of adoption, while the computer took 10 years and the smartphone 5 years.3 Adoption is growing especially in user demographics. Millennials lead with 95% overall adoption, but baby boomers are the fastest growing group, with their usage doubling from 39% to 79%.4 For certain demographics, fintech usage approached and exceeded traditional banking usage in 2021.

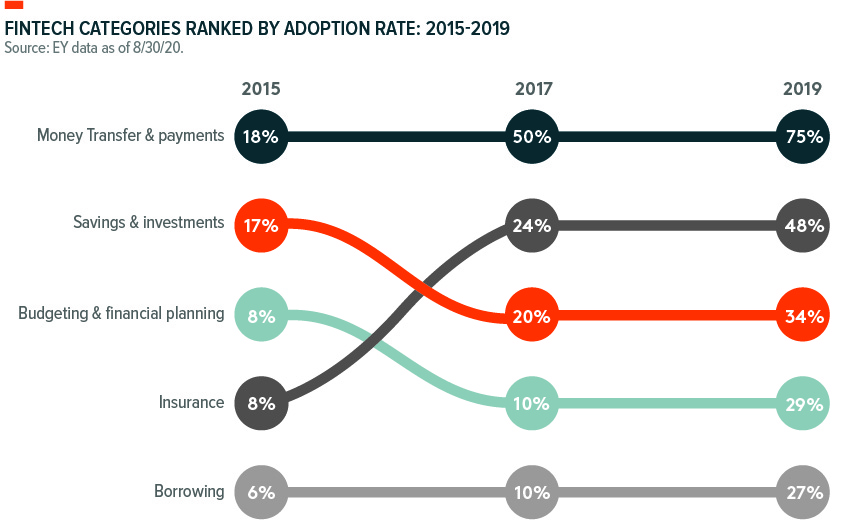

Based on available data, the global adoption rate of fintech solutions reached 64% in 2019.5 Innovations in mobile payments, online banking and alternative lending platforms can provide financial services to previously non-banking and underserved populations in emerging and emerging markets. Without existing infrastructure, such as traditional bank branches and credit cards, these markets can integrate the latest technology without forcing an old business model into obsolescence. Of the emerging markets, China and India have the highest adoption so far, with 87% in 2019.6

The chart shows the trend in fintech adoption worldwide for various traditional financial services prior to the pandemic. And it’s reasonable to assume that adoption has increased across all categories since the pandemic.

Blockchain can be a gateway to financial inclusion

In the most basic sense, a blockchain is a type of database aimed at capturing and maintaining data. Its unique features stem from its decentralized approach. Data is recorded in blocks on a digital ledger. Participants, called nodes, are the computers and devices connected to the network that distribute and validate the ledger on a peer-to-peer (P2P) network. While anyone can create data on public blockchains by creating a new block and linking it to a previous block, the consensus-based approach to validation means that no one can edit or falsify the data after it has received enough block confirmations. The result is a structure that inspires trust without the involvement of a third party.

Since participants don’t have to trust a government to back a currency or manage the money supply, it’s conceivable that blockchain networks will eventually become embedded in the financial ecosystem. This technology provides a mechanism for financial inclusion, especially in countries struggling with political instability, corruption or severe inflation.

A February 2021 survey found that the top 10 countries with the highest frequency of cryptocurrency use among their populations were all emerging markets. Nigeria led the way with 32% of respondents reporting that they use bitcoin or cryptocurrency more widely, followed by Vietnam at 21% and the Philippines at 20%.7 In the US, an estimated 16% of adults own cryptocurrency.8 We expect this number to increase over time, but investors should be cautious in the crypto space as regulation remains light and illegal activity is common. Consumer risk is likely to be a headwind for adoption. Scams, theft and volatility are risks. In 2021, $7.8 billion in value was defrauded and $3.2 billion in cryptocurrency stolen.9.10

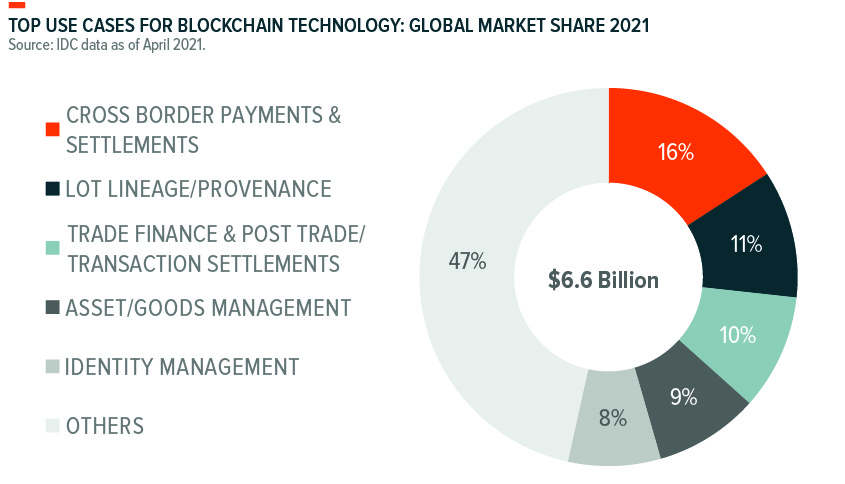

Beyond financial use cases, blockchain technology applications include huge, moving supply chains, healthcare tracking, and smart contracts.

Fintech is a crossroads for thematic disruption

A key advantage for fintech platforms compared to their more traditional financial competitors is their ability and willingness to integrate new approaches at scale and shift their business models as new technologies emerge. The merger of blockchain and fintech to form decentralized finance (DeFi) is a prime example. As a result, fintech is a natural crossroads for disruptive themes, including Internet of Things (IoT), Cloud Computing and Video Games.

Fintech platforms combined with IoT technologies can transform everyday services. For example, insurers typically work with incomplete information, which increases the cost of property and casualty insurance. But if they could use telematics sensors to track GPS and on-board diagnostic information, they could get more accurate information for insurers and potentially lower costs and faster solutions.

Cloud technology can streamline previously cumbersome processes for banks, such as onboarding new customers, opening accounts and managing regulatory compliance. Globally, the IT cloud spending of the banking sector is expected to grow at a CAGR of 16.2% between 2019 and 2024, rising to about 25% of IT budgets.11

Another new frontier for Fintech is gaming to earn with non-fungible tokens (NFTs). According to one estimate, by October 2021, more than 1 million digital wallets per day were connected to decentralized gaming apps, representing 55% of the blockchain industry’s total activity.12 These blockchain games enable the possession of playable items and therefore the ability to sell, trade, use and lend these tokens.

Putting the Fintech and Blockchain Themes in a Portfolio Context

Fintech will continue to digitize and make financial services more scalable. The transformation is immediately apparent, but also one that has significant scope to execute globally, as no use case exceeds 70% penetration.13 Crucially, as blockchain technology grows out of its infancy, we expect the reach of end-users and institutional applications to grow exponentially and potentially undermine traditional finance.

In our view, thematic stocks should be targeted, using screens to ensure the underlying companies provide the desired exposure. This pure play focus minimizes overlap between themes while distinguishing the exposure the theme provides over broad beta products.

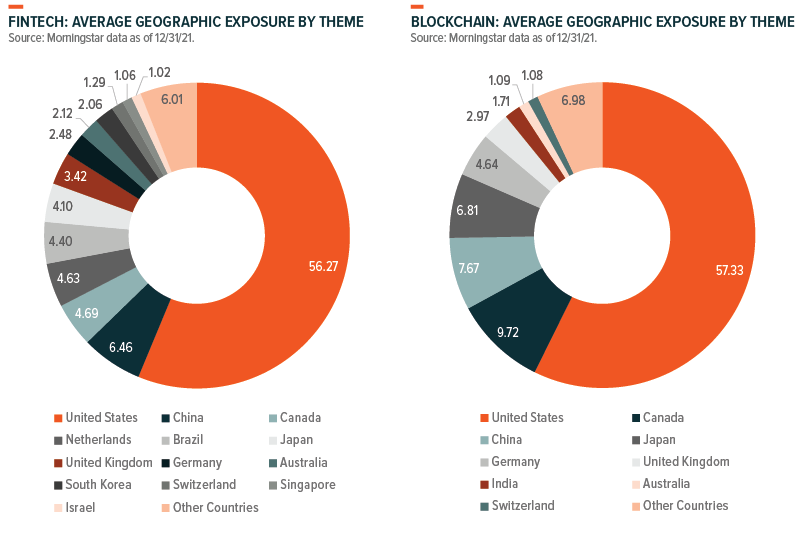

The companies operating in the fintech and blockchain spaces are global and positioned to benefit as thematic adoption increases across the globe. We believe there is a lot of innovation happening outside the US and limiting exposure to the US will exclude key players, which is detrimental to investors in the long run. The charts below summarize the geographic exposure of the largest fintech and blockchain-themed ETF products.

Note: Includes the five broad Fintech ETFs and the top five blockchain ETFs according to our thematic classification. All thematic ETFs weighed the same.

As blockchain remains in the innovation phase, the number of pure play blockchain companies is limited. Therefore, many ETFs include major semiconductor manufacturers that design and build crypto mining infrastructure. These companies are also included at a relatively high level in market capitalization weighted broad beta and technology sector ETFs. Over time, we expect the levels of overlap to decrease as the space matures and the number of pure play companies grows.

Conclusion: Fintech revolution in full swing

Actual paper money transfers may approach relic status as fintech shifts the way the world accesses and handles money. As the space advances and adoption grows, we believe that blockchain-based digital ledgers are likely to become the dominant way in which people send, manage, invest and lend. The rise of the digital payments segment to mass adoption levels illustrates the willingness of consumers to embrace these new technologies. Given the huge growth potential for fintech applications, we believe that a risk for investors is not being exposed to the Fintech mega-theme and the many investment themes it links together.

0 Comments