PeoplePictures

International game technology PLC (NYSE:IGT) recently gave a favorable outlook, noting that the numbers tend not to be so affected by global recessions. Given the amount of money invested in product development and new jurisdictions accepting online gaming, revenue growth plausible. I also believe that the separation of the Digital & Betting business segment could be very beneficial to the company’s valuation. Yes, there are risks, but the IGT share price is not expensive at all.

IGT

International Game Technology PLC is a world leader in game products from slot machines and lotteries to sports betting.

Source: company website

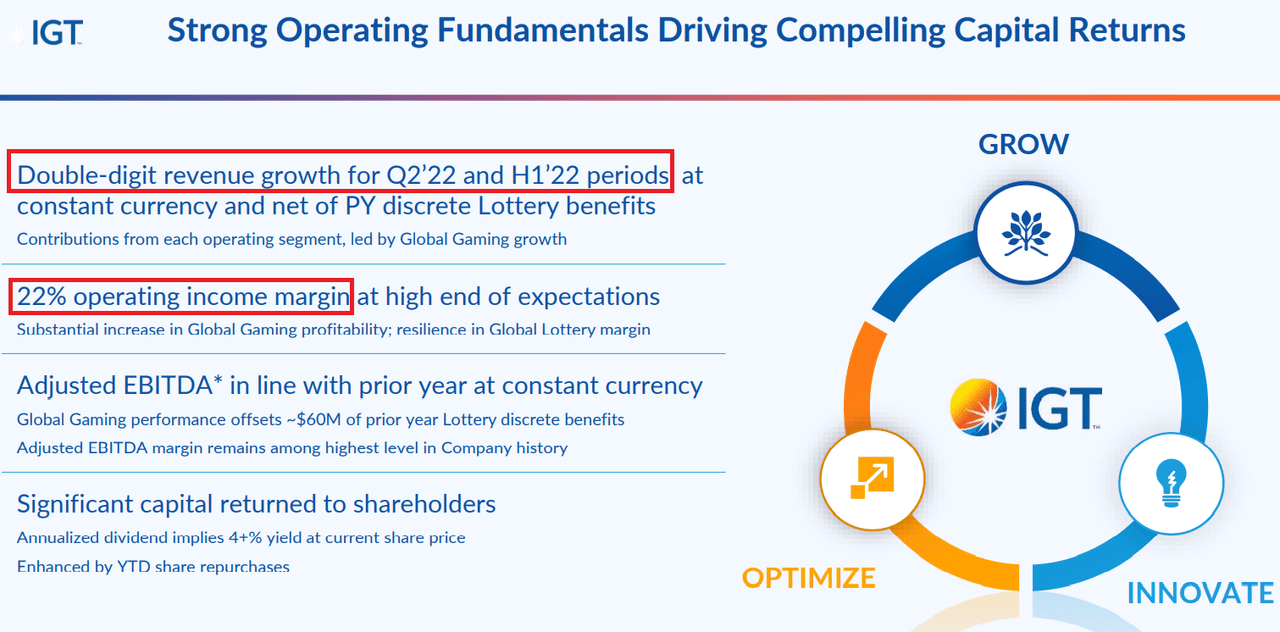

I became very interested in IGT’s company profile after reviewing the company’s most recent numbers. With global gaming growth leading other business segments, IGT reported double-digit revenue growth for the second quarter of 2022 and the first half of 2022. Management also reported an impressive 22% margin of operating income.

Source: Quarterly Presentation

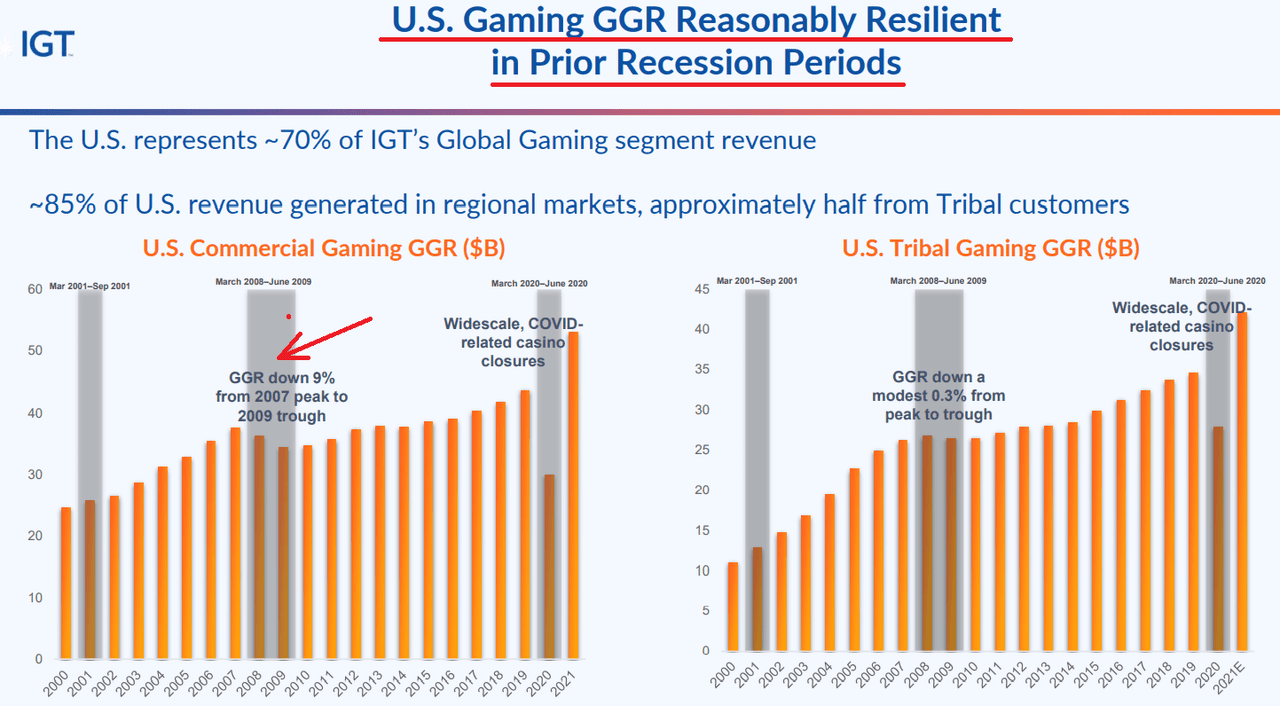

Since many economists note that a recession could occur, a position in IGT is worth considering. Keep in mind that the company’s business model has behaved quite well during recessions in the past.

Quarterly presentation

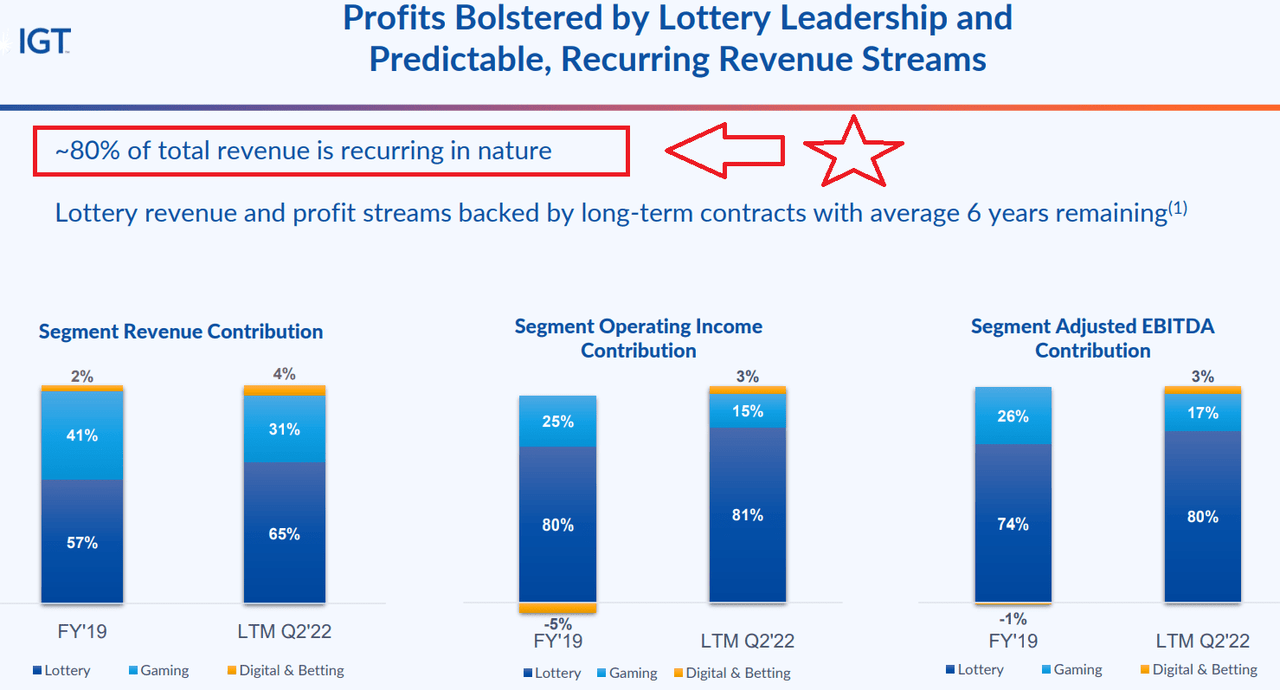

It is also very beneficial that IGT reports an impressive 80% recurring revenue, mainly thanks to the company’s lottery business segment and gaming. Recurring earnings are like music to my ears because predicting free cash flow is easy.

Quarterly presentation

Expectations include revenue growth, free cash flow growth and a small increase in capital expenditures

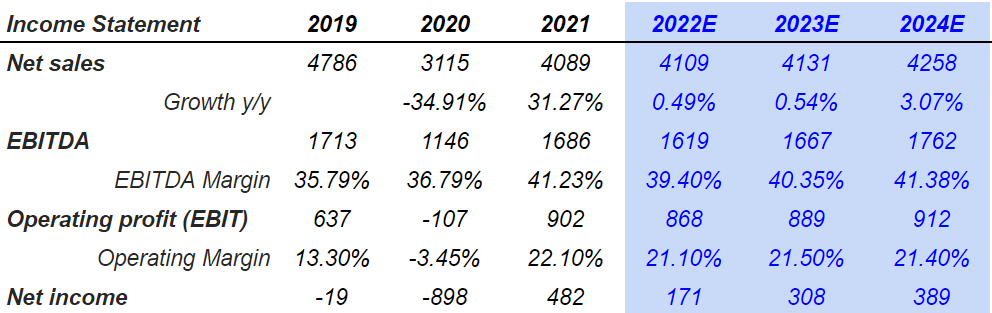

In my opinion, investors will most likely look at other analysts’ expectations before looking at my numbers. Market estimates include revenue growth in 2022 of 0.49% and revenue growth in 2023 of 0.54%. The EBITDA margin for 2022 and 2023 would also remain around 39% and 40%, and the net profit would most likely remain positive in 2022, 2023 and 2024.

Source: Marketscreener.com

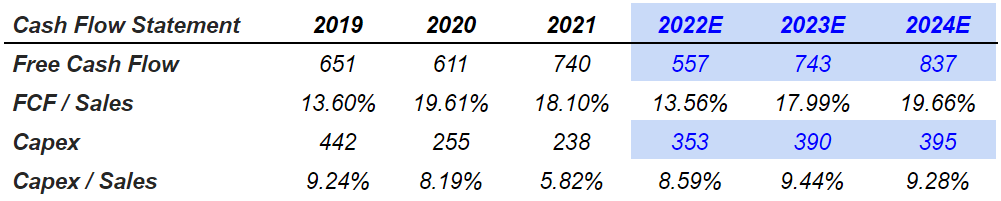

With regard to the cash flow statement, there is a lot to enjoy. Analysts believe the FCF will grow from $557 million in 2022 to $743 million in 2023 and $837 million in 2024. It is worth noting that capex is not expected to decline from 2022 to 2024. The increase in free cash flow is not caused by a drop in capex.

Source: Marketscreener.com

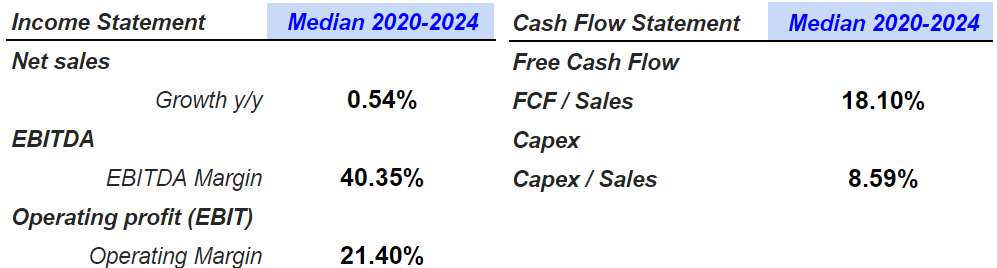

I’ve been trying to get some numbers from investment analyst numbers. The median figures include net sales growth of approximately 0.54%, EBITDA margin of 40% and free cash flow/sales of 18%.

Author’s Compilations

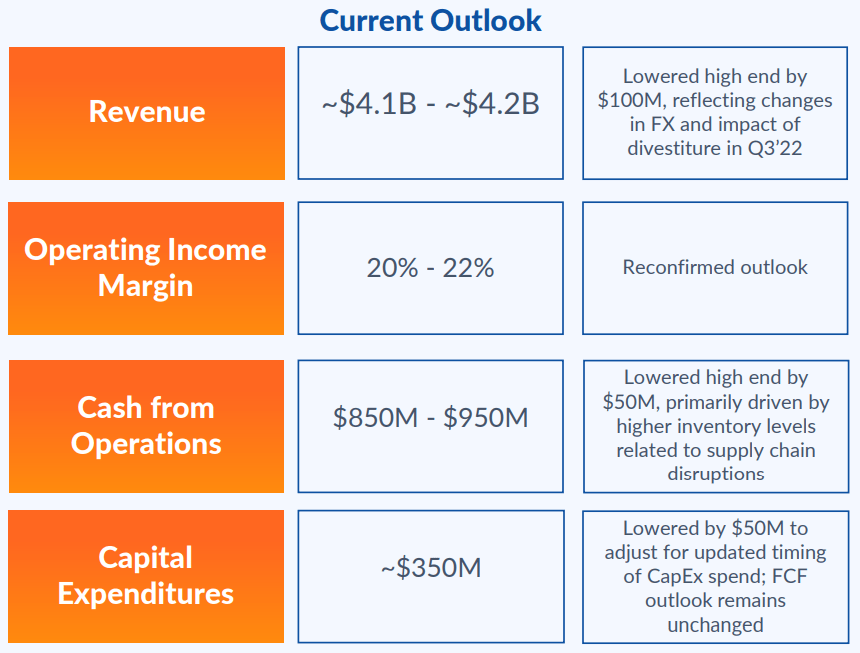

Management’s prospects are also optimistic. Future sales are expected to be close to $4.1 billion with an operating profit margin of 20% and a capital investment of approximately $350 million. I don’t think management’s numbers differ much from other financial advisors.

Quarterly presentation

Balance

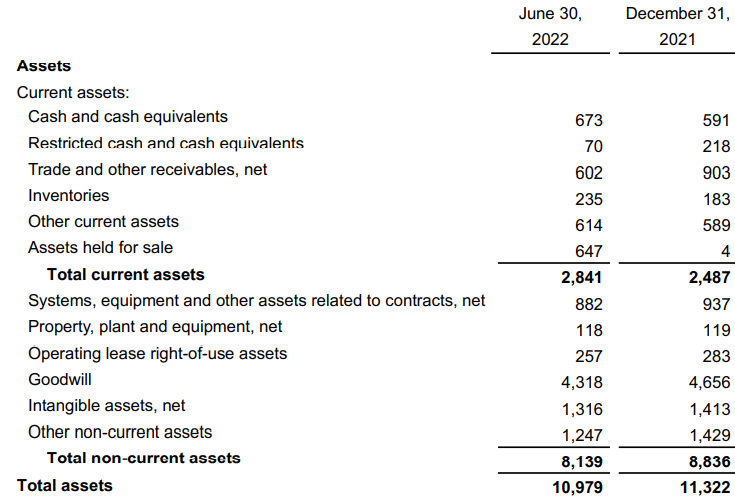

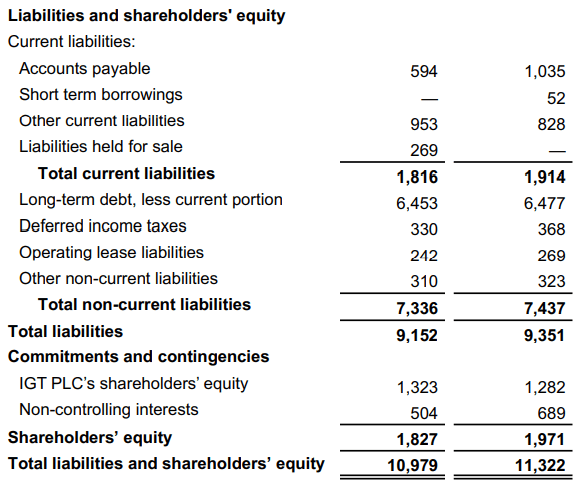

As of June 30, 2022, IGT has $673 million in cash and an asset/liability ratio of nearly 1x. Goodwill and intangible assets represent almost 51% of the total amount of assets. Therefore, I believe that impairment of intangible assets can have significant impact on the company’s balance sheet.

10-Q

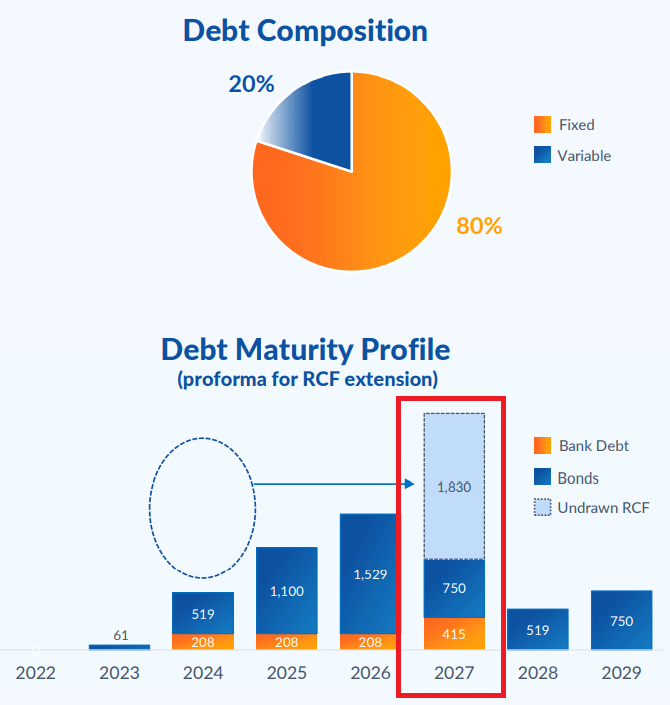

The long-term debt is $6.45 billion, which is not small at all. However, the company will have to pay most of its debt in 2027. I think IGT can generate enough free cash flow in the future to renegotiate its debt with bankers.

10-Q Quarterly presentation

Further product development, new mobile phone apps and the separation of the digital and gambling business segments could mean a valuation of $18.64 per share

In my opinion, if the growth of sports betting in the US continues thanks to regulations in new states, IGT will most likely benefit. I also believe that greater efforts to develop new mobile phone apps for each state are likely to increase revenue. There is no reason to believe that new mobile apps and game products will not succeed. Keep in mind that the company uses a significant amount of R&D expenditure and product development.

The company devotes significant resources to research and development, making $238 million, $191 million, and $266 million in related expenses in 2021, 2020, and 2019, respectively. Source: 20-F

I’m also quite optimistic about management’s plans for the Digital & Betting business segment. If this business segment is really sold on its own, then in my opinion, the valuation of the company could be more important than that right now. Keep in mind that the Digital & Betting business segment is growing faster than the other business segments. If financial advisors run a financial model of each business segment, the overall valuation may be greater than assessing IGT’s business model as a whole. In its most recent annual report, the company explained its plans:

As part of this process, the Company may evaluate a potential separate public listing of its Digital & Betting business segment to further enhance its strategic flexibility while maintaining a controlling interest following the completion of such potential separate public listing. No guarantees can be made as to the form and timing of any separate public listing or other strategic activity that may result from this review, or whether such listing or activity will be completed at all. Source: 20-F

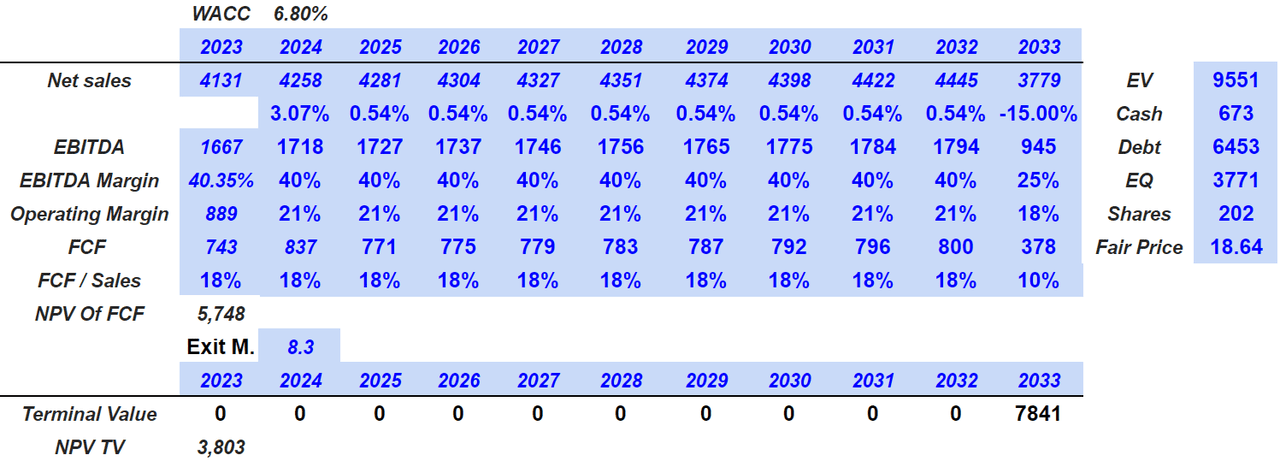

With a revenue growth of almost 0.54%, which is close to the median growth obtained previously, I achieved revenue growth of approximately $4 billion. It is approximately the estimate given by management. If we also use an EBITDA margin of 40%, an operating margin of 21% and an FCF/Sales of approximately 18%, 2033 would be FCF $378 million. Now, if we add up the future free cash flow from 2024 to 2033 at a 6.8% discount, the net present value equals $5.74 billion.

To calculate the terminal value, I used an exit multiple of 8.3x, which meant a net present value of $3.8 billion. With $673 million in cash and debt of approximately $6.45 billion, the equity valuation would be $3.7 billion and the fair price would be $18.64.

Author’s DCF Model

Problems with lottery authorities, changes in industry reputation and slow changes in new jurisdictions could lead to a valuation of $8.35 per share

Lottery authorities can terminate contracts signed by IGT for a variety of reasons, including failure to approve required budget appropriations or irreparable breaches. Given the total amount of revenue from the lottery segment, termination of contracts would destroy the company’s business model and revenues would fall:

Many of these contracts in the US allow the lottery authority to terminate the contract at will with limited notice and do not specify the compensation the company would be entitled to if such termination occurred. Source: 20-F

Changes in customers, consumer confidence and many other economic factors can also affect the company’s ability to generate revenue. Also, political conditions can alter society’s general perception of the industry. As a result, IGT can suffer reputational damage and lose business partners.

Management also expects changes in new jurisdictions to lead to new markets and revenue growth. If these processes take longer than expected, earnings expectations could fall, which could lower investor expectations. Worst case scenario, I think a drop in free cash flow expectations would lead to a drop in stock price.

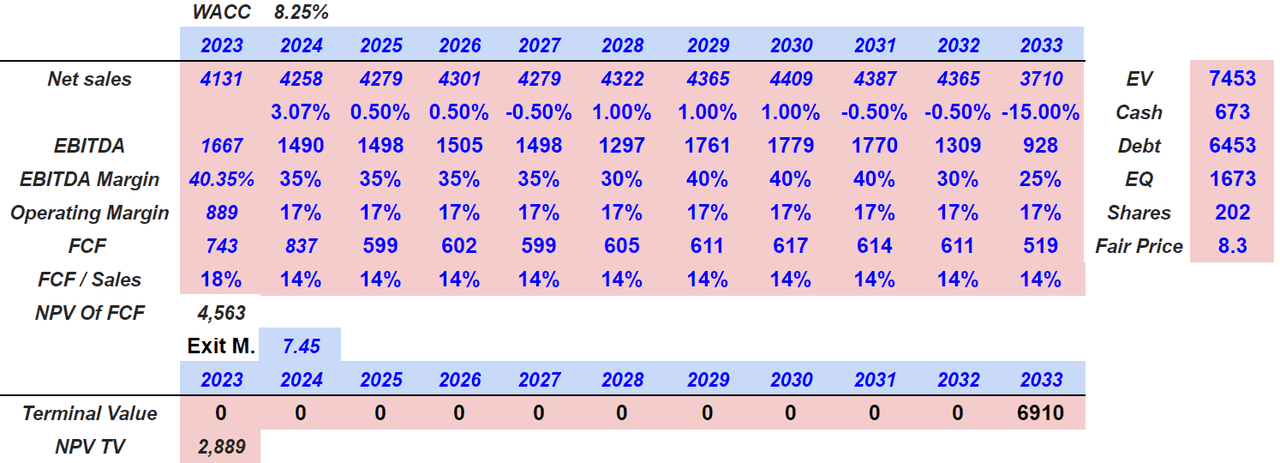

Assuming a scenario with revenue growth of around 1% and -0.5%, operating margin close to 17.5% and FCF/Sales of 14.5%, the sum of the FCF would be $4 .5 billion. Note that my margins are significantly lower than those in the previous scenario. I also used an 8.25% discount, which is more significant than the one in the base case. In my opinion, a drop in margins would lead to a higher cost of equity as traders can sell some of the equity.

If we include an exit multiple of 7.45x, which is below the industry median, the NPV of the terminal value is $2.895 billion. Finally, the enterprise value would remain close to $7.5 billion and the equity valuation close to $1.65 billion. The fair price would be $8.35 per share.

Source: SA Author’s DCF Model

Best Case Scenario: IGT Signs Another Agreement in Italy and Signs More Agreements in Europe

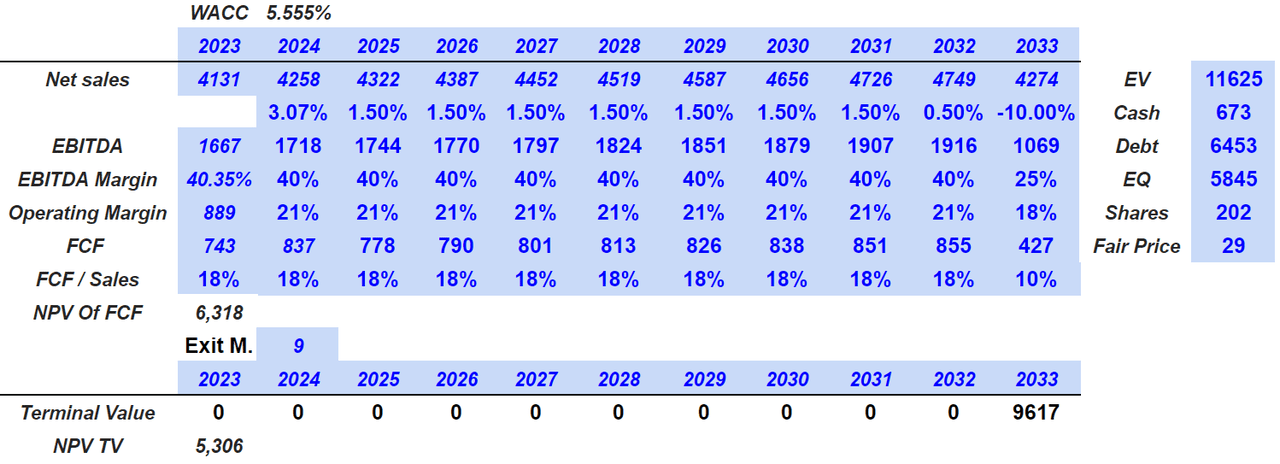

At my best, I’ve included two main assumptions. First, the company’s recent acquisitions would end well. The company would report no impairment of goodwill and future synergies will be realized. In addition, I assumed that the company would sign a new agreement in Italy, and perhaps much more in Europe. Under these optimistic conditions, some economies of scale would improve the company’s EBITDA and FCF margins.

Since 1998, and for a term expiring in 2025, the company has been the exclusive licensee for the Italian Lotto game. As of November 2016, the company’s exclusive license to the Italian Lotto includes partners as part of a joint venture. Lottoitalia srl, a joint venture between IGT Lottery SpA, Italian Gaming Holding as Arianna 2001 and Novomatic Italia, is the exclusive manager of the Italian Lotto game. Source: 20-F

In this case, I used 1.5% revenue growth, EBITDA margin of about 40% and FCF/sales of 18.2%. With a WACC of 5.55% and an exit multiple of nearly 8.95, the implied enterprise value would be $11.625 billion. Now if we subtract the debt and cash, the equity would be about 5.85 billion and the fair price would be $29.1 per share.

Author’s DCF Model (Author’s DCF Model)

Conclusion

IGT has provided helpful guidance. I believe that new mobile phone apps and new products can be expected. Ultimately, management invests a significant amount in research and development. The potential corporate reorganization that would separate one of IGT’s business segments is also worth considering. In my view, the overall valuation could be greater after the separation of the Digital & Betting business segment. Even taking regulatory risks into account, I believe IGT is worth more than its current price level.

0 Comments